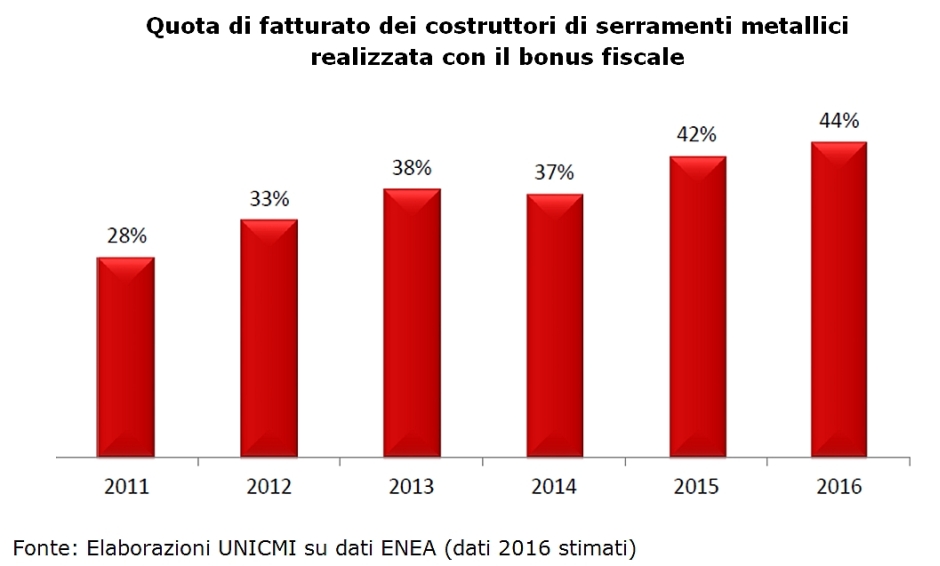

We asked Daniela Percoco, Real Estate Market Analyst, to provide a brief overview of the Italian construction and fixtures market. In a nutshell, there is a slight improvement in the Italian economy and a subtle upswing in the construction market. The tax bonus for energy redevelopment is fundamental for doors and windows. Indeed, 44% of the total demand for aluminium fixtures comes because of the tax incentives.

In a world economy seeing a growth trend, even if still below the medium- to long-term levels, the Italian macroeconomic situation is also showing indications of an awakening, even if at a rather limited pace. Improvements to the economic tune is evidenced by an upward revision of forecasts from the main economic institutes – for the first time since 2011.

For Italy, in the 2017–2018 two-year period, the recovery that started in 2014 was consolidated with an expected 1.3% growth in GDP for 2017 and 1.1% for 2018 (Centro Studi Confindustria). Whilst the signs of crisis remain profound, the general economic context has significantly improved since the summer of 2016, with progress having continued and been accentuated in the first half of 2017, following that observed at an international level (and at a European one in particular), where there are signs of a new investment cycle.

The construction sector, as a fundamental pillar of the national economy, has reversed course. For the first time since the beginning of the crisis, the ANCE forecasts on construction investments are no longer preceded by a negative but show an increase of 0.3% assumed for 2016 and 0.8% for the current year. These are still very timid increases that underscore the lasting uncertainty that continues to characterise the sector.

According to such indications, the only segment that will still be affected by negative changes in 2016 and 2017 is represented by new-construction housing, which has seen a loss of more than 60% since the beginning of the negative cycle. Conversely, ordinary maintenance operations have marked a growth of 19% compared to 2008 and now represent 37% of total building investments made (bearing in mind that in 2008, these comprised less than 20% of the total).

The trend of the doors and windows market is grafted onto this general context. In 2016, the overall demand for doors, windows and curtain walls in the Italian market reached a value of approximately 4.27 billion euro, of which 2.75 was in the residential sector and 1.52 in the non-residential sector. From 2012 onwards, a relative stabilisation of turnover was observed for both market segments whilst in 2016, there was a slight upswing in turnover in the residential market, which should continue in 2017. However, it should be noted that almost 80% of the items sold are destined for renewal works. Doors and windows sold for new buildings suffered a sharp contraction from 2008 to 2015, only to pick up slightly in 2016.

From 2017 to 2008, there was a gradual change in market shares (in terms of value) for the three main materials utilised to produce the fixtures (aluminium, wood and PVC). Plastic windows and doors showed significant growth, going from a market share of 16% to a market share of 26%. The growth in the market share of PVC windows and doors was also favoured by the lower average selling price, especially when compared with the price of fixtures in other materials with the same thermal performance required to access the tax benefits.

The market share of aluminium doors and windows is characterised by a slightly downwards trend and stands at 36%. Wooden windows and doors underwent a significant decrease in the market share value, going from 45% to 38%, mainly caused by competition from PVC windows. The analysis of market shares in terms of volumes highlights the leading position of PVC with a share of 34.2%, followed by aluminium doors and windows with a share of 33.1%, and those in wood with 32.7% of sales.

The tax incentives for the energy requalification of buildings contributed to significantly supporting the demand for doors and windows, generating cumulative sales of over 1.70 billion euro in 2016. It is estimated that some 70% of PVC window and door sales are made with the contribution of tax incentives, for a value of approximately 670 million euro in sales.

The impact of tax incentives on the aluminium windows and doors market has grown steadily since their introduction and today represents 44% of the total demand for aluminium fixtures, at a value of approximately 600 million euro.

{kind=link}